July 4, 2026

The Role of Permit in Renovation Loan Approval

The Role of Permit in Renovation Loan Approval

A building permit is the document lenders require to confirm that renovation work meets local safety codes, zoning rules, and construction standards before they approve or release funds. Without it, your renovation loan stalls. Florida homeowners and real estate investors face this reality on every project that goes beyond cosmetic work. The role of permit in renovation loan approval is not a technicality. It is the foundation lenders use to assess risk, protect collateral, and decide whether to write the check.

What types of renovations trigger a permit requirement in Florida?

Renovations requiring permits in Florida include structural changes, square footage additions, and any work touching electrical, plumbing, HVAC, mechanical, or gas systems. These categories cover most major renovation projects. Florida’s hurricane code requirements add another layer, meaning work that affects roof structures, windows, or exterior walls often triggers permit requirements that other states do not impose.

Projects that typically require a permit in Florida:

- Structural changes such as removing or adding walls

- Room additions or garage conversions that increase square footage

- Electrical panel upgrades, rewiring, or new circuit installations

- Plumbing changes including new fixtures, drain lines, or water heater replacements

- HVAC system replacements or new duct installations

- Roof replacements, especially those affecting structural components

- Window and door replacements in hurricane impact zones

- Decks, fences above a certain height, and accessory structures like sheds

Cosmetic projects are generally exempt. Painting, flooring, cabinet replacements, and minor landscaping do not require permits in most Florida jurisdictions. The line between cosmetic and structural is where homeowners most often make mistakes.

Pro Tip: If your contractor says a project “probably doesn’t need a permit,” get that in writing and verify it yourself with Miami-Dade’s permit office or through the Miami-Dade permit guides on Miamipermitai before work starts.

How do building permits affect renovation loan approval and disbursement?

Lenders treat unpermitted work as a liability, not an asset. Appraisers disregard it entirely when calculating property value, which directly lowers your loan-to-value ratio and can disqualify you from financing. A renovation loan tied to unpermitted work is a loan built on a foundation the lender cannot verify or insure.

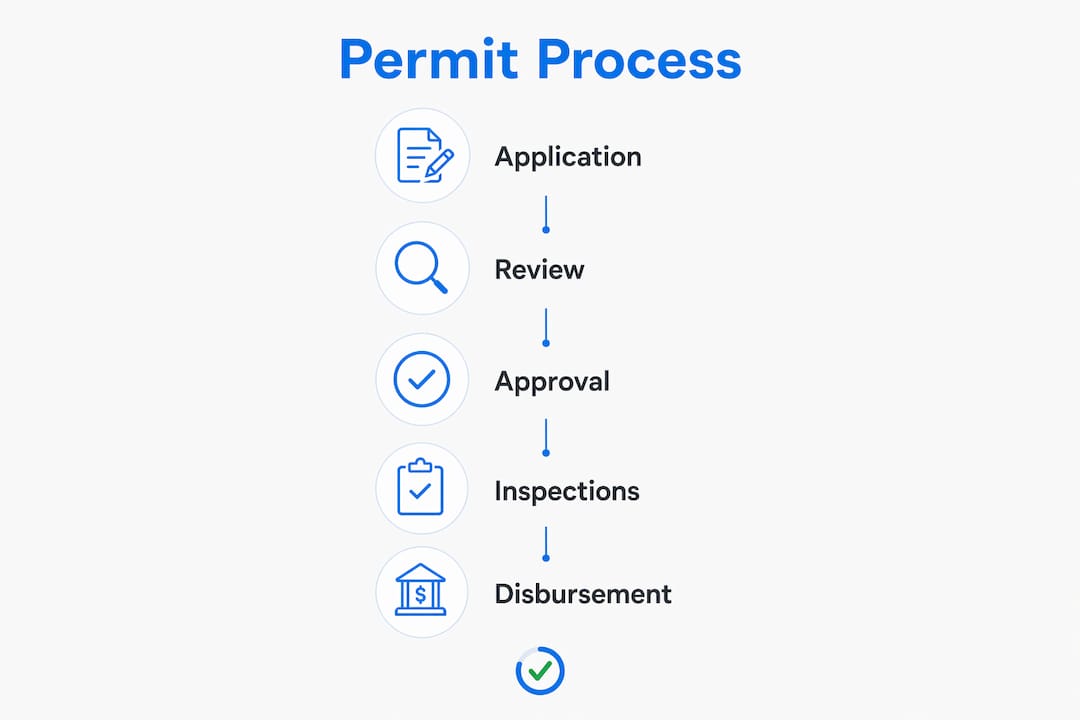

The process for permit-linked loan disbursement follows a clear sequence:

- Permit application submitted. The lender requires proof that permits are applied for or approved before construction begins.

- Written permit issued. Verbal approvals are insufficient for lender acceptance. Freddie Mac guidelines and most conventional lenders require written documentation.

- Construction begins. Work proceeds under the permit, with required inspections scheduled at each phase.

- Inspections passed. The lender or its designated inspector verifies that work meets code at each milestone before releasing the next draw of funds.

- Final inspection completed. The permit closes, and the lender releases the final disbursement.

For FHA 203(k) renovation loans, all work must comply with local building codes and required permits must be obtained and posted before construction begins. This is a hard requirement, not a suggestion. Missing a single inspection can freeze your draw schedule for weeks.

Open permits from previous owners create a separate problem. Unresolved permits from prior renovations obstruct loan approval until they are closed. In Florida, you must review local permit records before purchasing a property or applying for renovation financing. An open permit signals to the lender that prior work may not have passed inspection, which raises questions about the property’s code compliance status.

Pro Tip: Before you close on a property in Miami-Dade, run a permit history check. Miamipermitai pulls public Miami-Dade records and flags open or unresolved permits so you know exactly what you are inheriting.

What is the role of permit costs in renovation budgeting?

Permit fees in Florida are a real budget line, not an afterthought. Florida permit fees generally range from $150 to $2,500 depending on project scope and hurricane code compliance requirements. As a rule, permit fees represent roughly 0.5%–2% of total construction costs. On a $150,000 renovation, that means $750 to $3,000 in permit fees alone.

The fee itself is only part of the picture. Soft costs such as architectural plans and engineering reviews can add $1,500 to $10,000 before a single nail is driven. These costs are often invisible in early budget conversations, which is why so many renovation projects run over budget before construction even starts.

| Cost Category | Typical Range | Notes |

|---|---|---|

| Permit application fee | $150–$2,500 | Varies by project scope and jurisdiction |

| Architectural or engineering plans | $1,500–$10,000 | Required for structural and major system changes |

| Permit delay carrying costs | $3,000–$5,000 per six weeks | Added mortgage interest during construction hold |

| Retrofitting unpermitted work | 2–4x original permit cost | Penalty multiplier for after-the-fact permits |

Delays are the hidden cost most homeowners underestimate. A six-week permit delay can add $3,000 to $5,000 in additional mortgage carrying costs. That figure often exceeds the permit fee itself. The financial impact of a delayed permit is not the fee. It is the interest, contractor downtime, and extended loan draw period that stack up while you wait.

Budgeting for permits early also strengthens your financing position. Lenders look more favorably on renovation budgets that include permit costs as explicit line items. It signals that the borrower understands the full project scope and has planned for compliance from the start.

- Include permit fees as a named line item in your renovation budget

- Request soft cost estimates from your architect or engineer before finalizing the loan amount

- Ask your lender how permit delays affect your draw schedule and interest accrual

- Factor in the cost of retrofitting if any prior unpermitted work is discovered

Common pitfalls in managing permits during renovation loans

The most expensive permit mistake homeowners make is assuming the contractor handles everything. Contractor bids frequently omit permit fees, leaving homeowners responsible for costs they never anticipated. Always verify whether permit fees appear as a named line item in the bid and confirm in writing who is responsible for pulling the permit and scheduling inspections.

Licensed contractors are generally responsible for pulling permits in Florida. When a homeowner pulls a permit instead, they assume legal liability for the work and risk complications if the project later needs to be sold or refinanced. Florida’s DBPR contractor license verification exists precisely to protect homeowners from unlicensed work that cannot be properly permitted.

Starting construction before permits are issued is another common error that stalls renovation loans. Lenders conduct progress inspections tied to the permit record. If work begins without a permit, the lender has no verified baseline for the project, which can freeze disbursements or trigger a stop-work order from the county.

Pro Tip: Track your permit status actively, not passively. Miamipermitai monitors permit progress through Miami-Dade’s public records and sends email updates so you always know where your permit stands before your next draw request.

Best practices for keeping your renovation loan on track:

- Verify open permits on any property before purchase or loan application

- Confirm that your contractor is licensed through Florida DBPR before signing a contract

- Require written permit documentation before construction begins, not verbal assurances

- Schedule inspections proactively to avoid gaps in the draw timeline

- Keep a copy of all permit approvals, inspection reports, and correspondence with the county

Key Takeaways

Building permits are a non-negotiable requirement for renovation loan approval because lenders use them to verify code compliance, protect collateral value, and control fund disbursement at every stage of construction.

| Point | Details |

|---|---|

| Permits gate loan disbursement | Lenders release funds only after inspections tied to the permit pass at each construction phase. |

| Unpermitted work kills loan value | Appraisers ignore unpermitted work, lowering property value and loan-to-value ratios. |

| Open permits block financing | Unresolved permits from prior owners must be closed before a new renovation loan can be approved. |

| Soft costs add up fast | Architectural plans and engineering reviews can add $1,500–$10,000 before construction starts. |

| Written permits are required | Verbal approvals from local authorities or HOAs do not satisfy lender documentation requirements. |

What I’ve learned about permits and renovation loans in Florida

Most homeowners treat the permit as a bureaucratic box to check. That framing costs them money. The permit is actually the financial spine of a renovation loan. Every draw, every inspection, every appraisal ties back to it. When the permit process breaks down, the loan breaks down with it.

The investors I respect most in Florida treat permit readiness the same way they treat title insurance. They get it done early, they verify it thoroughly, and they never assume the contractor has it covered. The ones who skip that discipline are the ones calling me six weeks into a project wondering why their lender froze their draw.

Florida’s hurricane code requirements make this even more consequential than in other states. A roof replacement that would be a simple permit in Ohio becomes a multi-inspection process in Miami-Dade, with wind mitigation requirements and FEMA flood zone considerations layered on top. Underestimating that complexity is how renovation budgets blow past their loan limits.

The practical advice I give every homeowner: pull the permit history on any property before you commit to a renovation loan. Open permits from prior owners are far more common than people expect, and they are almost always cheaper to resolve before closing than after. Miamipermitai makes that check straightforward for Miami-Dade properties, grounding the review in real folio records and Miami 21 zoning data.

Permits also protect your exit. When you sell or refinance, the buyer’s lender will ask the same questions your lender asked. A clean permit record is a selling point. An unpermitted addition is a negotiating liability that can kill a deal at the worst possible moment.

— Leo

How Miamipermitai supports your renovation loan readiness

Permit problems are easier to prevent than to fix. Miamipermitai reviews your building permit package against Miami-Dade requirements before you submit to the county, flagging missing documents, plan inconsistencies, and the issues most likely to cause rejections or delays.

For homeowners and investors preparing for a renovation loan, that pre-submission review means fewer surprises during lender inspections and a cleaner draw schedule from start to finish. Miamipermitai grounds every review in Miami 21 zoning, FEMA flood zone data, folio property records, and Florida DBPR contractor license verification. You get a readiness score, a clear list of what to fix, and plain-language guidance you can act on immediately. Check your permit before you submit and protect your financing timeline from the start. For a deeper look at what triggers rejections in Miami-Dade, the permit rejection guide on Miamipermitai covers the most common failure points in detail.

FAQ

Do lenders require permits for all renovation loans?

Most renovation loan programs, including FHA 203(k) and Freddie Mac ChoiceRenovation, require permits for any work that affects structure, systems, or safety. Cosmetic work such as painting or flooring is generally exempt.

What happens if a renovation has unpermitted work?

Lenders and appraisers disregard unpermitted work when valuing the property, which lowers the loan-to-value ratio and can disqualify the renovation loan entirely.

Can an open permit from a prior owner block my renovation loan?

Yes. Open permits from previous renovations must be resolved before a lender will approve a new renovation loan on the property.

How do permit costs factor into a renovation loan budget?

Permit fees in Florida typically represent 0.5%–2% of construction costs, and soft costs like architectural plans can add $1,500–$10,000 on top of that. Both should be included as explicit line items in your loan budget.

Who is responsible for pulling permits on a renovation project?

Licensed contractors are generally responsible for pulling permits in Florida. Homeowners who pull permits themselves assume legal liability for the work and risk complications during future sales or refinancing.

Recommended

Is your permit package ready?

Run an AI readiness check against Miami-Dade requirements before you submit.

Try your first analysis freeThis article is general guidance and not legal, engineering, or official county advice. Always verify requirements with Miami-Dade County before submitting a permit.